1 rok temu

1 rok temu

Blackstone Sees AI Revolution Growing Private Credit Market To Staggering $25 Trillion

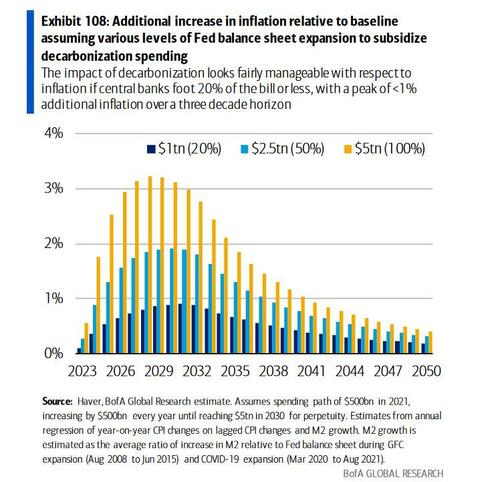

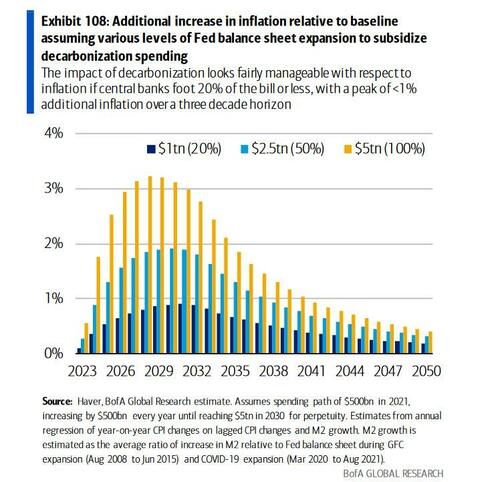

Several years ago we calculated that the cost to implement the „Green new deal”, and to fund the liberal crusade against „climate change” would cost no less than $150 trillion over 30 years, or about $5 trillion per year, a staggering amount, and one which would require constant QE by central banks in the trillions each and every year to have any chance of ever getting funded, a process which just incidentally would spark double (if not triple) digit inflation.

Which of course was the whole point: the bullshit „green” narrative was spewed by the top echelons of power not because these private jetsetters give a rat’s ass about the environment – if that was the case the CO2 footprint of the top 1% would not be greater than the bottom 90% – but because they always needed a palatable and „virtuous” justification to spend like drunken sailors, be it to destroy ideological enemy X in noble war Y (where the deep state is the biggest beneficiary of the flood in defense spending), or to destroy evil climate change.

Now, it is well-known that the framework for this gargantuan spending spree took place „before covid”, a world which was largely devoid of inflation and where there were tens of trillions in negative-yielding bonds – hardly the stuff that allows debt to be inflated away, in fact quite the opposite – and since the goal was precisely that, namely to inflate away the world’s hundreds of trillions in excess debt, the „unexpected but welcome arrival” of the covid crash and the runaway inflation that the resulting fiscal spendgasm unleashed, effectively obviated the green new deal. No longer would the world need to justify spending $150 trillion to „fix climate” in order to spark the runaway inflation that would inflate the world’s record debt.

But the presence of inflation eliminating the core need for the „climate change” crusade, also meant that suddenly there was a gaping hole for what the „next big thing” would be that would require trillions in (preferably taxpayer-funded, i.e. QE) spending, that would then by quietly transferred into the pockets of middlemen who took it upon themselves to „effectively” allocate said capital.

Enter the AI narrative.

Yes, just like Blu Rays, 3D TVs, 3D printers, the 5G revolution, and so many other gimmicks over the recent years, the true purpose of AI – which is nothing more than a glorified yet prone to catastrophic error and hallucination chatbot – is to force management teams (and taxpayers) to spend capex like drunken sailors, in the process creating a new order of ultra rich entrepreneurs, who return the favor and allocate purchase orders to the same management teams, while making the insurmountable moat separating the tech giants from the rest of the market even wider. In short: all AI does is create the illusion of some huge, unmet market (some idiots have even mentioned quadrillions in Total Addressable Market size) while in realty what it really does is allocate capital to a handful of soon to be super wealthy scam artists, while leaving the population – and gullible creditors – holding the bag when this latest ivory tower comes crashing down. But don’t take our word: here is Goldman expressing skepticism about the next big thing (full note available to pro subs in the usual place).

And while much of the equity has already been distributed to the lucky few, with Nvidia and OpenAI by far the biggest winners and with the „Next AI trade” – namely the energy infrastructure needed to keep all those thousands of electricity-guzzling data centers up and running – waiting in the wings for its day in the sun and your brokerage account, where the real bonanza will be is not equity at all but rather debt.

We touched upon this two weeks ago when we reported that according to Morgan Stanley, „The AI Revolution Will Unleash An Explosion In New Debt Issuance„.

Quoting the bank’s head of quantitative research, Vishwanath Tirupattur, we said that „It goes without saying that AI infrastructure will need substantial capex. Early on, much of the AI capex has been funded by a combination of venture capital and retained earnings from cash-rich technology companies, i.e., equity capital. As the focus shifts from early innovators and enablers to AI adopters, these needs are bound to grow significantly and will require more efficient forms of capital. We think that credit markets in various forms – unsecured, secured, securitized and asset-backed – will have a major role to play.„

In addition, we noted, „as the capex cycle broadens out from enablers to adopters, we note that most sectors are not as cash-rich as tech. While the median cash-to-debt ratio for the tech sector is over 50%, it stands at close to 15% for the remaining sectors. As capital needs driven by the AI infrastructure build-out increase, we expect reliance on credit markets to grow.”

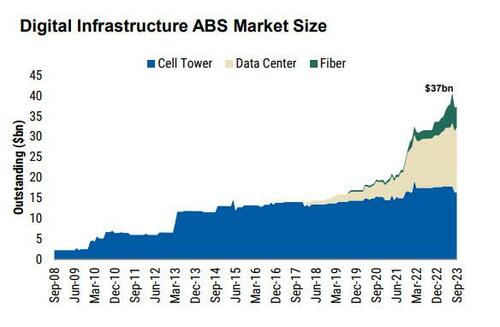

Financing for AI infrastructure, particularly data centers, will not come from corporate credit markets alone. Data centers can be owned by the companies using them or by a data center operator that leases space to them. The data centers themselves and/or the tenant lease payments can be treated as the underlying collateral to access securitization markets. This is already happening. The first data center ABS was issued in 2018, and the market has now grown to over US$20 billion and is poised for rapid growth.”

The bottom line, we said, is that „as AI-driven technology diffusion takes center stage, credit markets, broadly defined, will likely play a growing role. As always, there will be winners and losers, but AI as a theme for credit investors is here to stay.„

This may have been an understatement, because fast-forwarding to today, Blackstone Credit and Insurance’s global chief investment officer, Michael Zawadzki, said on Bloomberg Television that the $1.7 trillion private-lending industry is still “in batting practice” before it swells to a $25 trillion market.

And what will drive this expansion? Take a wild guess: according to Zawadzki, the funding needs will be to finance the energy transition (he didn’t get the memo yet that the „Green” narrative is dead) and – of course – data centers (this is the narrative that is now stepping in to justify the coming debt tsunami, now that the „green new deal” is dead).

“You’re financing the real economy — you’re not waiting for M&A transactions to happen,” Zawadzki said. “You’re financing consumers, you’re financing data centers, you’re financing energy transition. Huge growth capital expenditures, that’s what’s really driving the growth.”

And that’s how, when you repeat the lie enough times, a hallucinating chatbot becomes „the real economy.”

Higher base rates, the shift from banks to private lenders and the proliferation of strategies to access private credit allow the market to grow larger, Zawadzki said. The private investment grade strategies like asset-backed finance and infrastructure credit are “really compelling” in today’s market, he said. The size of the asset-based finance market is about $5 trillion to $10 trillion, he said.

Naturally, having become the largest commercial and residential landlord in the US, Blackstone is now seeking to monopolize the next big thing: data centers in general, and the private debt to fund them in particular. Not surprisingly the private equity giant has been active in the asset-based finance markets, leading debt packages for cloud computing firm CoreWeave tied to assets including microchips. And as is well known, CoreWeave has been one of the first and biggest drivers of growth at Nvidia (and we aren’t even going into the conspiracy theories). So, if one is so inclined, one can directly trace the flow of money: from Blackstone debt to CoreWeave purchase orders, to Nvidia AI chip backlogs, to trillions in market cap gained for a handful of firms, to the S&P and Nasdaq at daily all time highs.

Talk about leverage, and that is just the start.

Of course, it’s not just AI: Zawadzki said that spreads in public markets have become “awfully tight” due to investors flowing into the asset class. So Blackstone has encouraged clients to enter private credit due to excess spread and the illiquidity premium it offers. But credit is nothing without the demand for it, and right now, nothing screams demand more than AI and the need to fund the tens of trillions in infrastructure growth over the next few years.

Just don’t call it the „Green Next Deal.”

More: „The AI Revolution Will Unleash An Explosion In New Debt Issuance.”

Tyler Durden

Tue, 07/02/2024 – 15:45