1 rok temu

1 rok temu

Inflation Expectations Will Keep Rising In 2025, And It Matters Most In Japan

By Dhaval Joshi, chief strategist at BCA Research

Executive Summary

- In the developed economies excluding Japan, rising inflation expectations will lift them further above the 2 percent target. This will limit the scope for further interest rate cuts.

- But in Japan, rising inflation expectations will lift them up to the BoJ’s 2 percent target. This will remove the BoJ’s justification for its decades-long zero interest rate policy (ZIRP).

- The normalisation of Japan’s monetary policy poses a big risk to stocks because Japan has been the main source of financial market liquidity, and thereby, of rising stock market valuations.

- Hence, the biggest risk to US tech valuations comes from a rise in the Japanese real bond yield.

- On a structural (1-2 year) time horizon though, it is highly likely that Japanese real yields will rise, causing a meaningful setback in stocks versus bonds, and especially the US superstar stocks.

- But from a timing perspective, wait until the complexities of the price trends in USD/JPY and/or Nasdaq versus 30-year T-bond have reached the point of collapse that signalled previous reversals at the end of 2023 and the summer of 2024. You can monitor these indicators on our website.

- Go tactically long copper.

2024’s political Zeitgeist was encapsulated in what I have called the ‘3 I’s’: Incumbents punished for Inflation and Immigration.

Incumbent governments were given a kicking by furious electorates who had suffered a huge drop in their standard of living. And it made not the slightest difference whether the incumbents were left-of-centre Democrats in the US, centrist Macronists in France, or right-of-centre Conservatives in the UK.

In the case of excess immigration, the loss of well-being was feared. In the case of excess inflation, the loss of well-being was genuine. Yet since peaking in 2022 at close to 10 percent, inflation has plunged to the low-single digits. So, why is everybody still so angry?

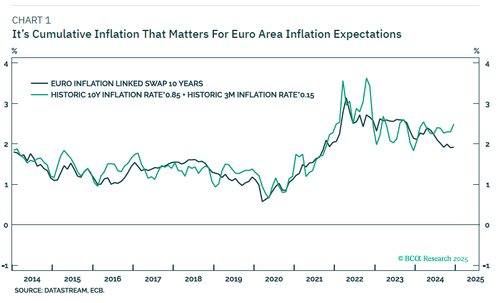

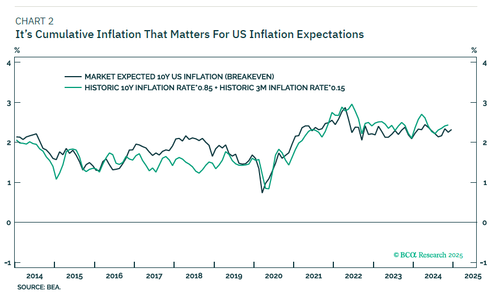

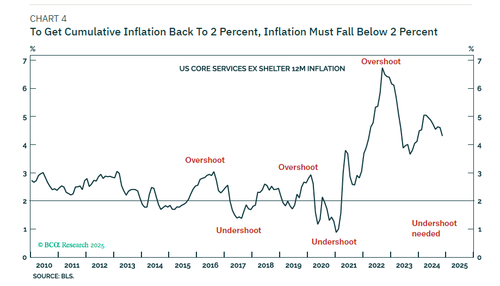

It’s Cumulative Inflation That Matters

One of the main reasons that central banks target 2 percent inflation is that 2 percent is the highest rate of inflation that goes largely unnoticed. Going largely unnoticed, households and firms do not consciously factor sub-2 percent inflation into their price and wage setting processes. This prevents an ‘inflation spiral’ taking hold.

The reason that sub-2 percent inflation goes largely unnoticed is that economic productivity also tends to rise at 1-2 percent. And to the extent that wages rise in line with productivity, people will not suffer a loss of purchasing power when prices rise at 2 percent or below. So, the inflation goes unnoticed.

The thing that people notice and hate, is the cumulative loss of purchasing power when prices keep rising at above 2 percent.

Telling people that inflation is back down in the low-single digits will not make them feel any better when they have just suffered a cumulative loss of purchasing power of 25 percent!

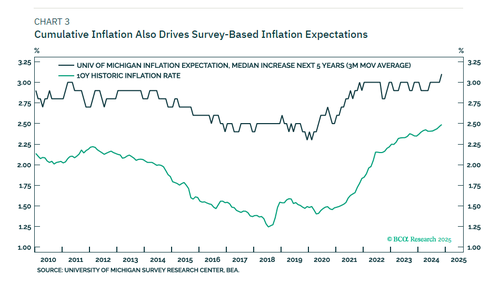

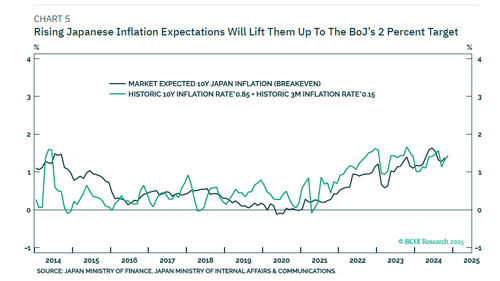

It is this cumulative effect of past inflation that sets inflation expectations. As the charts in this report show, market expected 10-year inflation is nothing more than historic 10-year inflation (with a small tweak for the very recent inflation experience)

But what about survey-based inflation expectations? The answer is that survey-based inflation expectations like the University of Michigan consumer survey of 5–10-year US inflation expectations also track delivered long-run inflation (albeit, plus a constant).

Hence, to get cumulative inflation back to the 2 percent rate that is unnoticeable, inflation must fall below 2 percent to offset the post-pandemic period when inflation was running well above 2 percent. But as central banks are unlikely to take inflation much below 2 percent, inflation expectations – as a mathematical identity – will trend higher

Put more simply, inflation expectations will trend higher because the post-pandemic noticeable inflation era will become a greater part of our collective experience compared with the pre-pandemic unnoticeable inflation era.

Or, more precisely, inflation expectations will trend higher unless they cause a deflationary shock (or an exogenous deflationary shock arrives) that wrench them lower again. Such a shock might come from Japan.

Japanese Inflation Expectations Are Approaching Mission Accomplished

In the developed economies excluding Japan, rising inflation expectations will lift them further above the 2 percent target. This will limit the scope for further interest rate cuts, for two reasons. First, because it risks further un-anchoring those inflation expectations.

Second, because it is the real bond yield that matters for the economy. If inflation expectations rise, then nominal bond yields must also rise to achieve a given real stance of monetary policy. This means that bond yields will trend higher until the shock arrives that wrenches them lower. In Japan though, rising inflation expectations will lift them up to the BoJ’s 2 percent target.

Mission accomplished, it will remove the BoJ’s justification for its decades-long zero interest rate policy (ZIRP), especially with the real bond yield now deeply negative. It may sound perverse after decades of too low inflation, but once inflation is close to target, a deeply negative real bond yield risks taking Japanese inflation too high.

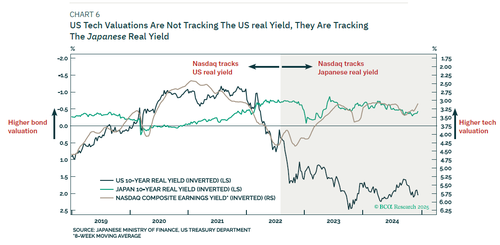

The Normalisation Of Japan’s Monetary Policy Poses A Big Risk To Stocks

The normalisation of Japan’s monetary policy poses a big risk to stocks because Japan has been the main source of financial market liquidity, and thereby, of rising stock market valuations.

Through 2019-2022, the Nasdaq’s valuation (earnings yield) moved in perfect lockstep with the US real bond yield, as might be expected. But in late-2022, the Nasdaq’s valuation detached from the US real yield and attached to the world’s last remaining negative real bond yield – in Japan.

Hence, through 2023-2024, the Nasdaq’s earnings yield has moved in near-perfect lockstep with the Japanese real bond yield. This means that the biggest risk to US tech valuations does not come from a rise in the US real bond yield. The biggest risk comes from a rise in the Japanese real bond yield. This also solves the seeming mystery as to why the US tech valuations have been largely unscathed by the recent surge in the US real bond yield. To reiterate, US tech valuations are not tracking the US real yield, they are tracking the Japanese real yield. US tech valuations have been largely unscathed because the Japanese real yield has not surged… yet.

On a structural (1-2 year) time horizon though, it is highly likely that Japanese real yields will rise. This will end the major source of financial market liquidity that is behind the powerful yet narrow 2023-24 surge in stock market valuations. On this structural (1-2 year) time horizon therefore, I expect a meaningful setback in stocks versus bonds, and especially the US superstar stocks.

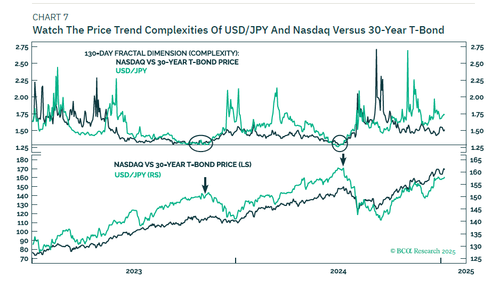

But from a timing perspective, wait until the market has become too dovish on the BoJ and/or too bullish on the US superstar stocks. In other words, when the complexities of the price trends in USD/JPY and/or Nasdaq versus 30-year T-bond have reached the point of collapse that signalled previous reversals at the end of 2023 and the summer of 2024.

These excellent timing indicators are not yet flashing red. The good news is that you can monitor them updated daily on our website.

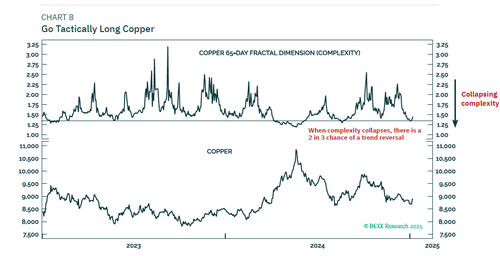

Go Tactically Long Copper

Finally, relating to trend changes among the major investments and sectors we monitor, there is a tactical buying opportunity for copper.

The recent sell-off in copper has reached the collapsed short-term complexity that has signaled stabilisations and rebounds through 2023-24.

Tyler Durden

Sun, 01/12/2025 – 18:40