9 miesięcy temu

9 miesięcy temu

Energy Price As An Economic Indicator

Authored by Lance Roberts via RealInvestmentAdvice.com,

What are energy prices telling us about the economy? A recent article on Bloomberg noted that:

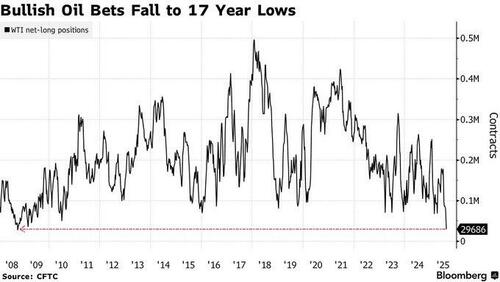

“Hedge funds slashed their bullish position on crude to the lowest in about 17 years as risks of additional sanctions on Russian crude oil waned, bringing concerns about a global supply glut back to the fore. Money managers’ net-long position on West Texas Intermediate shrank by 19,578 lots to 29,686 lots in the week ended Tuesday, data from the Commodity Futures Trading Commission show. That’s the lowest since October 2008.”

However, there is more to this story than just easing global tensions and rising oil supplies impacting energy prices. Energy prices indicate economic strength, or, in this case, weakness. If the global economy grew strongly, the need for oil consumption would rise, absorbing the current production levels, causing energy prices to rise. However, the outlook for economic growth in the major oil consumption economies, the U.S. and the Eurozone, is very weak.

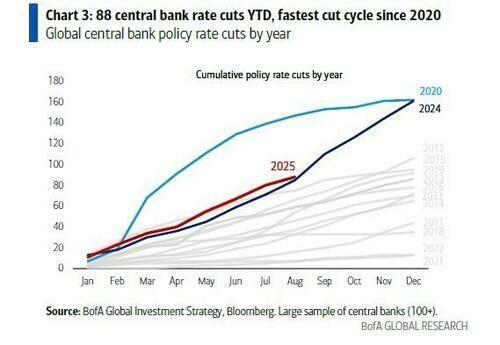

This is also why we are seeing the fastest pace of Central Bank rate cuts since the pandemic crisis in 2020, and the Federal Reserve in the U.S. is now joining in despite record-high stock markets.

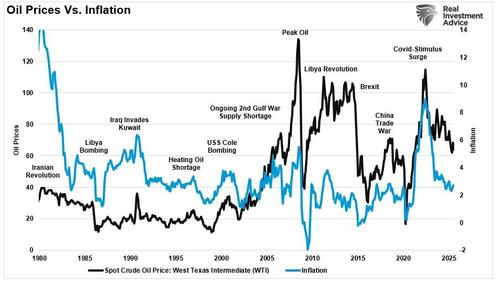

However, I would be remiss in not stating that energy prices are susceptible to “geopolitical shocks.” This is because NYMEX traders bid up oil prices in anticipation of oil shortages, or conversely, excesses, but these price fluctuations tend to be shorter-term events.

Over the longer term, energy prices are an indicator of economic strength or weakness. This is because, as noted previously, energy is consumed in every part of the economic cycle.

“High oil prices add to the costs of doing business which pass, ultimately, on to customers and businesses. Whether it is higher cab fares, more expensive airline tickets, the cost of apples shipped from California, or new furniture shipped from China, high oil prices can result in higher prices for seemingly unrelated products and services.” – Investopedia

Of course, consumers who fill up their gas tanks each week immediately notice high oil prices. While core inflation reports strip out food and energy, those items drive short-term consumption patterns. Given that consumption comprises roughly 70% of the GDP calculation, the impact of higher oil prices is almost immediate.

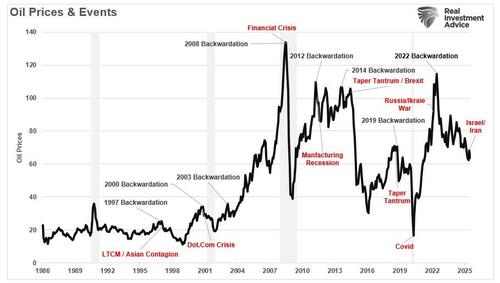

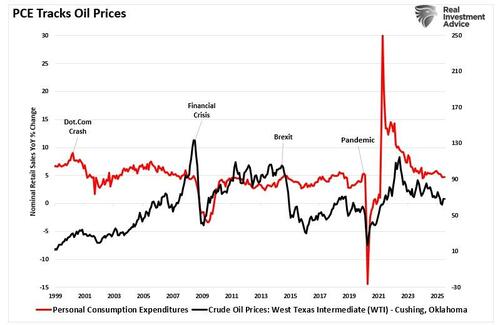

As shown above, spikes in oil prices are highly correlated with economic recessions, financial events, and oil price reversions. Therefore, let’s explore energy prices as an economic indicator to see what oil is currently telling us about the state of the U.S. economy.

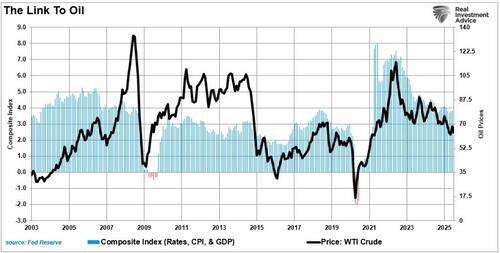

The Link To Oil

As noted, energy prices are crucial to the overall economic equation. As prices increase, consumers face higher inflationary costs. Unsurprisingly, there is a high correlation between the rise and fall of energy prices and the consumer price index. Unsurprisingly, energy prices and inflation have declined as economic demand weakened following the 2020-2021 stimulus-driven economic growth surge.

Since energy prices feed into virtually every aspect of our lives, from our food to the products and services we buy, we can expand our view of oil as an economic indicator. Therefore, the demand side of the equation is a tell-tale sign of economic strength or weakness. The chart below uses an economic composite of GDP, interest rates, and inflation compared to oil prices. It would be unsurprising that there is a decent correlation between the two.

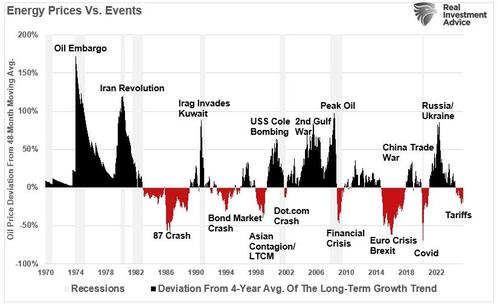

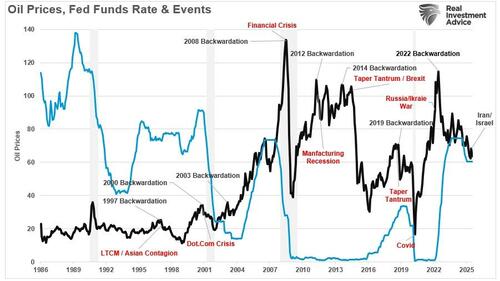

Since the oil industry is manufacturing and production-intensive, falling energy prices impact other economically important facets of manufacturing, employment, and capital expenditures. The chart below shows oil prices and events relative to the deviation from the 4-year average energy price. While geopolitical events spike energy prices, as is 2022, those spikes result in economic downturns, reducing demand, thereby lowering energy prices.

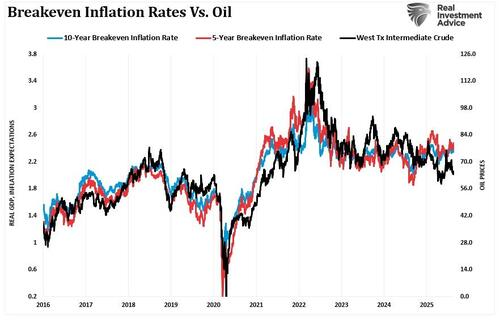

While the pandemic-driven shutdown of the economy created a supply shortage, the flood of liquidity inevitably created a demand surge. That “pull-forward” of consumption led to surging inflationary pressures and rising oil prices. We show the high correlation between oil prices and breakeven inflation rates.

Oil prices reflect overall economic activity, given their vast contribution to everything consumed. With liquidity reversing, economic demand is weakening as the cost of living outpaces real wages. As such, the correlation between declining energy price, future economic growth, and inflation breakevens should be unsurprising.

The Fed Should Pay Closer Attention To The Energy Price

As noted above, global central banks have been cutting interest rates at the fastest pace since the pandemic, as many of those countries teeter on the edge of recession. However, the Federal Reserve remained steadfast until recently that its concern was a resurgence of inflation due to tariffs. But, as noted above, energy prices warned that inflation is not a concern for the U.S., and the Fed may be behind the curve in cutting rates.

Given that consumption makes up ~70% of the GDP calculation, and the importance of oil in everything we consume, it should be unsurprising that oil prices also reflect economic activity in the aggregate. The current decline in energy prices says a lot about underlying economic strength, which the Fed noted has shown up in the latest employment data.

“In the near term, risks to inflation are tilted to the upside, and risks to employment to the downside—a challenging situation. When our goals are in tension like this, our framework calls for us to balance both sides of our dual mandate.” – J. Powell

However, as noted above, energy prices clearly show that inflation risks are tilted to the downside, with the larger risk being a much weaker economic growth rate. As such, the Federal Reserve should likely cut rates more aggressively now to avoid the potential warning from the decline in oil prices.

If energy prices reflect economic activity, then their current trend points to growing weakness beneath the surface of headline data. While equity markets reach new highs and unemployment appears low, the sharp drop in oil prices and declining breakeven inflation expectations tell a different story. It’s not geopolitics or supply excesses driving prices lower. It’s waning demand. And that’s a red flag.

The Fed’s delayed response to this signal is concerning. As Powell notes, their framework must balance inflation and employment. But right now, inflation pressures are easing, not accelerating. Oil prices reflect that shift more clearly than any lagging indicator. If consumption is slowing, and energy prices strongly suggest it is, then the Fed should move faster, not slower. Waiting for confirmation in backward-looking data risks compounding economic weakness already in motion.

Historically, when oil prices fall significantly, the economy follows. The Fed would do well to pay attention.

Tyler Durden

Fri, 08/29/2025 – 15:00