9 miesięcy temu

9 miesięcy temu

Beige Book Sees „Little Change” In Econ Activity: Notes Rising Wages As Immigrant Labor Shrinks While „Inflation” Mentions Tumble

Many were shocked (again) after the latest CPI and PPI data confirmed that the experts were once again dead wrong, and instead of the widely expected inflation tsunami, Trump’s tariffs have so far sparked only sporadic disinflation, which will only become more acute as the home prices slide accelerates. And yet, anyone who read our Beige Book analysis from April (not to mention our accurate prediction from last June that „The Experts Are All Wrong About Inflation Under A Trump Presidency”) would have known just that: as we laid out, „Beige Book Finds Inflation Mentions Tumble To 3 Year Low” which was the clearest indication that despite the prevailing narrative, rising prices is simply not a thing businesses across the US are worried about. We got further confirmation of this last month, when the latest Beige Book found no runaway inflation (again) but instead that sentiment in the economy splitting along party lines.

Fast forward to today when the latest, September, Beige Book was released, and it revealed that 8 of the 12 Fed districts reported „little or no change in economic activity since the prior Beige Book period” when as we reported then „economic activity increased slightly from late May through early July” , while four Districts reported „modest growth.” And yes, there were no regions reporting a slowdown, hardly the apocalypse so many liberals have been expecting. This is also a solid improvement from the May period, when the Beige Book found that half of Districts reported at least slight declines in activity.

The Beige Book noted that across districts, „contacts reported flat to declining consumer spending because, for many households, wages were failing to keep up with rising prices” and „contacts frequently cited economic uncertainty and tariffs as negative factors. New York reported that “consumers were being squeezed by rising costs of insurance, utilities, and other expenses.” Maybe New Yorkers should look for other cities in which to live then?

The Fed’s contacts also observed the following responses to the consumer pullback: retail and hospitality sectors offered deals and promotions to help price-sensitive consumers stretch their dollars, supporting steady demand from domestic leisure tourists but not offsetting falling demand from international visitors.

The auto sector noted flat to slightly higher sales, while consumer demand increased for parts and services to repair older vehicles. Manufacturing firms reported shifting to local supply chains where feasible and often using automation to cut costs.

Curiously, the Beige Book made its first mention of AI, saying that „the push to deploy AI partly explains the surge of data center construction—a rare strength in commercial real estate noted by the Philadelphia, Cleveland, and Chicago Districts. Atlanta and Kansas City reported that data centers had increased energy demand in their Districts.” Notably, it has also sent electricity prices soaring.

In one year, this will be the most popular chart on this site pic.twitter.com/h93gWXMoNL

— zerohedge (@zerohedge) August 11, 2025

Overall, sentiment was mixed among the Districts. Most firms either reported little to no change in optimism or expressed differing expectations about the direction of change from their contacts.

Focusing on labor markets, the Beige book reported the following:

- Eleven Districts described little or no net change in overall employment levels, while one District described a modest decline.

- Seven Districts noted that firms were hesitant to hire workers because of weaker demand or uncertainty.

- Moreover, contacts in two Districts reported an increase in layoffs, while contacts in multiple Districts reported reducing headcounts through attrition—encouraged, at times, by return-to-office policies and facilitated by greater automation, including new AI tools.

- Most Districts mentioned an increase in the number of people looking for jobs.

Notably, half of the Districts noted that contacts reported a reduction in the availability of immigrant labor, with New York, Richmond, St. Louis, and San Francisco highlighting its impact on the construction industry. And clearly tied to that, half of the Districts described modest growth in wages, while most of the others reported moderate growth.

As for prices, it should come as no surprise by now that the runaway inflation everyone was expecting just isn’t there. Here is Beige book confirmation

- Ten districts characterized price growth as moderate or modest. The other two Districts described strong input price growth that outpaced moderate or modest selling price growth.

- Nearly all districts noted tariff-related price increases, with contacts from many Districts reporting that tariffs were especially impactful on the prices of inputs.

- Contacts in multiple Districts also reported rising prices for insurance, utilities, and technology services.

- While some firms reported passing through their entire cost increases to customers, some firms in nearly all Districts described at least some hesitancy in raising prices, citing customer price sensitivity, lack of pricing power, and fear of losing business.

The best part: tariff deflation: „In some cases, as highlighted by Cleveland and Minneapolis, firms reported being under pressure to lower prices because of competition, despite facing increased input costs.„

In short, for yet another month, the sky is not falling.

Here is a snapshot of highlights by Fed District:

- Boston: Economic activity expanded slightly overall, but consumer spending was flat. Employment was down slightly, while wages and prices increased modestly. Home sales increased moderately from a year earlier. The outlook remained cautiously optimistic on balance, although tariff-related uncertainty dimmed the outlook for consumer spending.

- New York: Economic activity declined slightly as tariff-related uncertainty continued to weigh on businesses. Employment in the region was mostly unchanged, and wage growth remained modest. Selling prices rose at a moderate pace, marking some acceleration since the previous reporting period, and input prices rose strongly.

- Philadelphia: Business activity increased modestly in the current Beige Book period. Employment levels held steady, and wages rose at modest pre-pandemic rates. Firm prices rose moderately, straining budgets for many households and small businesses, and inflation expectations are higher still. In addition, tariffs and federal budget cuts are expected to add additional stress. Still, expectations for future growth broadened among most firms.

- Cleveland: Fourth District business activity increased slightly in recent weeks, and contacts expected activity to rise modestly in the months ahead. Manufacturers reported flat demand because of uncertainty, and retailers said sales were flat because of affordability concerns. Contacts said cost growth remained robust, while their selling prices increased modestly.

- Richmond: The regional economy grew modestly in recent weeks. Consumer spending drove the overall growth as activity in non-consumer facing sectors of the economy were flat to down slightly. In particular, manufacturing activity was down modestly this cycle. Employment levels were largely unchanged, and wage growth remained moderate. Price growth remained moderate, overall, despite some pickup in price growth in the services sector.

- Atlanta: The Sixth District economy declined slightly. Employment remained steady, and wage pressures moderated. Prices rose moderately. Consumer spending slowed, leisure travel fell, and business travel was flat. Home sales rose slightly; commercial real estate weakened. Transportation and manufacturing declined modestly. Lending at District banks increased. Energy activity rose.

- Chicago: Economic activity in the Seventh District increased modestly. Consumer spending increased moderately; manufacturing activity increased modestly; employment and business spending increased slightly; nonbusiness contacts saw no change in activity; and construction and real estate activity declined slightly. Prices rose moderately, wages rose modestly, and financial conditions loosened slightly. Prospects for 2025 farm income were unchanged.

- St. Louis: Economic activity and employment levels have remained unchanged while wages and prices have increased at a faster pace in the recent past. Contacts continue to express a high degree of uncertainty and concern about the impact of immigration policies on labor supply; they expect prices to accelerate over the next year due to tariffs. The outlook remains slightly pessimistic, but deterioration has subsided.

- Minneapolis: District economic activity contracted slightly. Employment fell as labor demand softened. Wage pressures were moderate, and prices ticked up modestly. Consumer spending fell as price sensitivity rose. Manufacturing also fell, with wide variation among contacts. Commercial and residential construction improved slightly, and home sales rose slightly. Agricultural conditions remained weak given poor commodity prices and despite good crop conditions.

- Kansas City: Economic activity was generally flat across the District. Employment declined modestly, and wage pressures remained subdued, although growth in non-wage benefit expenses caused total labor costs to rise. Input price growth was broad-based and contributed to moderate growth in selling prices, declines in profit margins, and expectations of sustained price pressures.

- Dallas: Economic activity in the Eleventh District economy rose modestly, buoyed by a pickup in nonfinancial services and manufacturing activity. Loan demand grew, but the housing market remained weak. Employment was flat and staffing firms noted slow hiring activity. Price pressures persisted, particularly in the manufacturing sector. Outlooks improved but there was widespread trepidation regarding shifting trade policy, high interest rates, and more restrictive immigration policy.

- San Francisco: Economic activity edged down slightly. Employment levels were down slightly. Wages grew somewhat, and prices rose modestly. Conditions in agriculture, retail trade, and consumer and business services sectors eased slightly. Manufacturing activity declined modestly. Conditions in residential and commercial real estate were largely unchanged, and lending activity was stable.

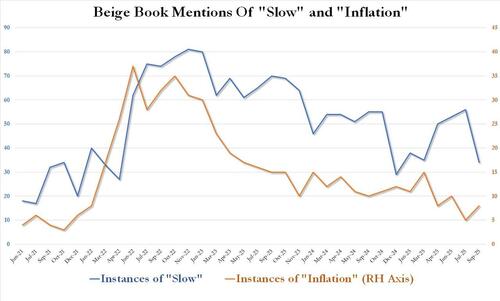

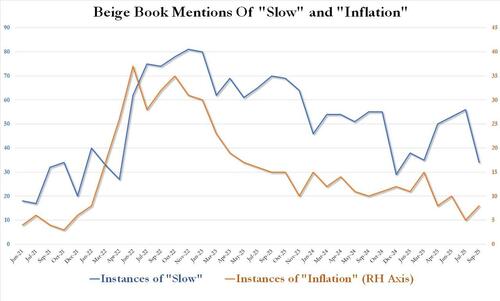

And finally, confirming that contrary to conventional wisdom the economic picture appears to have improved notably April, the latest Beige Book found that despite media narratives to the contrary, mentions of inflation remained near a 4 year lows, at just 8 in September, and up from the cycle low of 5 in July (effectively before the Biden inflationary explosion period) while mentions of „slow” tumbled from a two year high of 56 in July to just 34, indicating that according to the Fed respondents, neither inflation nor an economic are major concerns any more.

All of which suggests that the US economy – while hardly on fire as it was during the hyperinflationary period of Biden’s admin – continues to chug along and is hardly collapsing as so many Trump foes would like to see; and it certainly is not seeing prices explode higher.

Tyler Durden

Wed, 09/03/2025 – 15:00

![„Nowa żona” dryfuje bez „męża” po Zalewie Zemborzyckim. Poszukiwany właściciel [ZDJĘCIA]](https://cdn.spottedlublin.pl/media/2026/06/lodz_nowa_zona_dryfujaca_na_zalewie_zemborzyckim-ae952aeabd43.jpg)